We are publishing this month’s newsletter earlier than usual because of the market decline we’ve seen in the most recent 3 weeks. Volatility, fear, anxiety, and doubt are certainly back in the fold, and with them usually comes heightened emotions.

So, I wanted to chime in and offer some additional perspective to help alleviate any concerns you may have. While the recent declines have been unsettling for many, especially when the media seems to only cause more fear with their headlines, it’s important to remember that our GVCM strategies are designed to navigate times like these. In the midst of market uncertainty where headlines seem to be driving the market, we strive to maintain our focus on what the data is telling us because when emotions run high is when people usually make the wrong decisions.

So, let me start with our conclusion first: our GVCM strategies are still ‘risk on’, which means we are currently still in the market. And because the markets can turn in an instant, our strategies will also remain adaptable. Despite the heightened volatility and mixed economic signals such as the February employment report, our long-term outlook remains cautiously optimistic. But with the current concerns around tariffs, which also impact how the Federal Reserve acts, we do expect things to be sloppy and choppy for a while.

The recent volatility, primarily driven by tariff uncertainties and concerns around growth, is not unprecedented. In fact, we saw a similar market reaction when tariffs were imposed by President Trump in his first term back in 2018-2019. Initially, markets reacted strongly; however, each subsequent tariff threat or implementation had a lesser reaction as investors became accustomed to them or recognized they were not catastrophic.

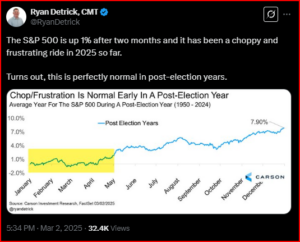

Ryan Detrick of the Carson Group, noted for his analysis and observations of market trends, was on a news channel appearance this past month and he mentioned that February following an election is often the worst month, while the first quarter following an election is typically the worst quarter, during a Presidential term. I also found his post below interesting:

Keep in mind that while Active management aims to minimize losses during downturns and capture gains during upturns, we always need to have a longer-term view. The reason is that a portfolio is usually comprised of different money managers, each of whom has their own methodologies and signals. Long-term strategies (such as GVCM’s) will hold through market declines until long-term signals indicate it’s time to exit, while shorter-term strategies tend to exit and re-enter more frequently as trends change. We diversify by using different non-correlated managers who manage their own respective portion of your account, and these managers will move at different times.

In response, our GVCM strategies earlier last week transitioned from a leveraged market exposure to a 1x market exposure for precautionary measures. This is a “step-down” resulting from our signals hitting an intermediate-term ‘sell’. Though still in the market, it’s now in a position where it can either move back into a leveraged position or conversely go on defense (cash and equivalents) depending on how the market evolves or devolves. I also want to note that even though there’s been an intermediate-term sell signal, it does not mean it will result in a long-term sell signal, as markets could turn on a dime. This is why our strategies remain adaptable.

So, to reiterate, our long-term signals are still bullish in the meantime but if market conditions further deteriorate and warrant that we go on defense, then our strategies will move as well. If you’d like to talk or do a review, please feel free to reach out to us at albanoteam@gvcaponline.com. Until next time.